18 min read • Last updated June 2026

Singapore's property market is a dynamic landscape, often segmented into three distinct regions: the Core Central Region (CCR), Rest of Central Region (RCR), and Outside Central Region (OCR). For both seasoned investors and first-time homebuyers, understanding the nuances of these regions is paramount to making sound investment decisions. While each region offers unique advantages and caters to different buyer profiles, the perennial question remains: Which Singapore property region offers better returns in 2026?

This comprehensive guide aims to demystify the CCR, RCR, and OCR classifications, providing an in-depth analysis of their historical performance, current market trends, investment potential, rental demand, and entry pricing. We will delve into common misconceptions and equip you with the knowledge to navigate Singapore's property market with confidence. By the end of this article, you will gain a clearer perspective on which region aligns best with your investment objectives, budget, timeline, and risk tolerance, empowering you to make an informed choice rather than chasing perceived trends.

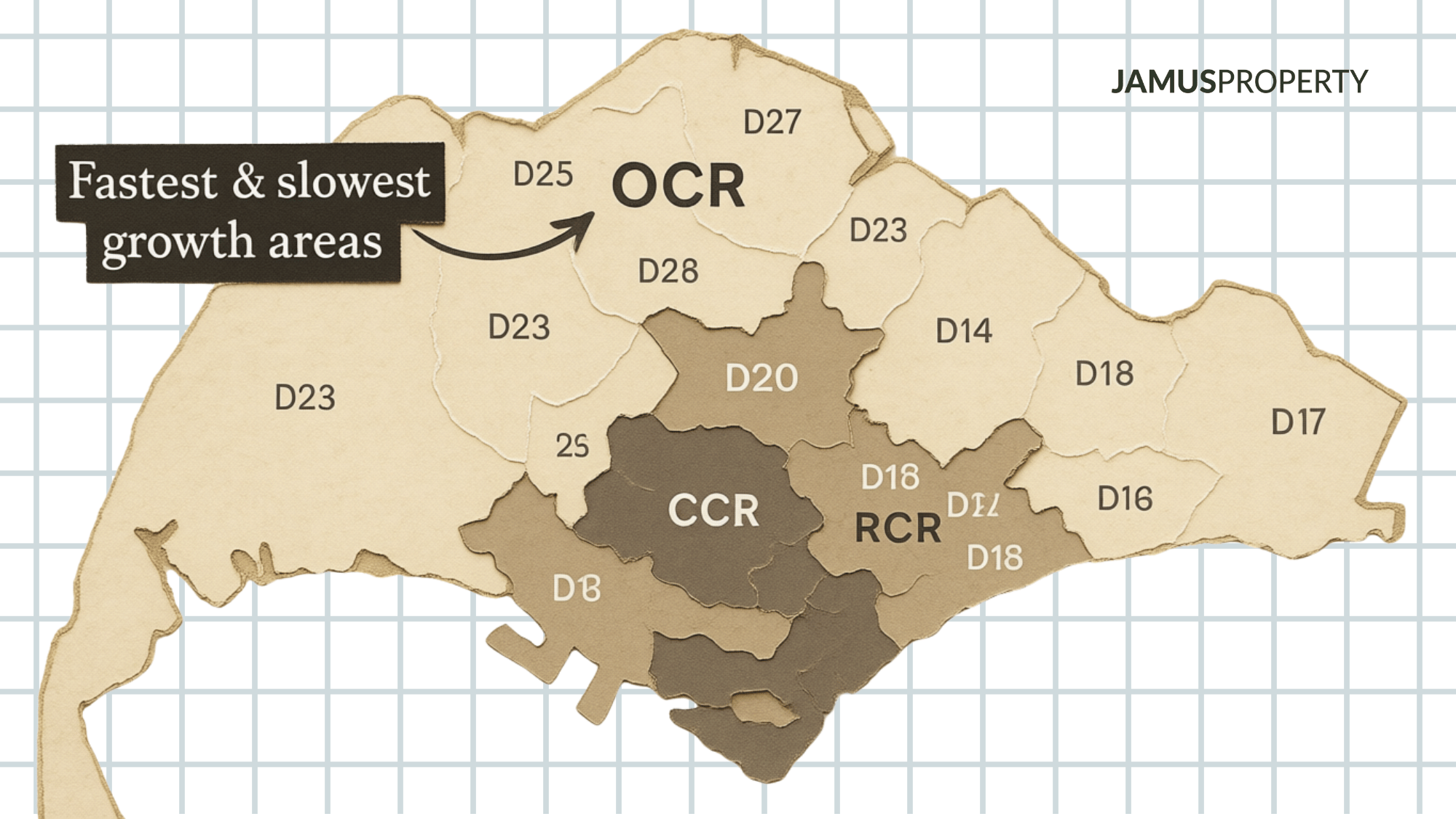

1. What Do OCR, RCR and CCR Mean?

Singapore's urban planning and property market analysis frequently categorize residential properties into three regions, a framework established by the Urban Redevelopment Authority (URA) to provide consistent benchmarks for comparison. These classifications are crucial for understanding market dynamics, pricing strategies, and buyer profiles.

Core Central Region (CCR): This encompasses the most prime and prestigious districts of Singapore, including postal districts 9, 10, 11, the Downtown Core, and Sentosa. Properties in the CCR are typically characterized by their proximity to the Central Business District (CBD), luxury amenities, and high-end residential offerings. The government's planning context for CCR emphasizes its role as a global city center, attracting high-net-worth individuals and expatriates. Typical buyer profiles include affluent local and foreign investors seeking capital preservation, prestige, and strong rental income from a discerning tenant pool.

Rest of Central Region (RCR): Often referred to as the city-fringe, the RCR includes districts such as 3, 4, 5, 7, 8, 12, 13, 14, 15, and 20. This region acts as a bridge between the prime CCR and the broader mass-market OCR. RCR properties offer a balance of accessibility to the city center and relatively more affordable price points compared to the CCR. Government planning in RCR focuses on developing vibrant urban hubs and residential enclaves that cater to professionals and families seeking a blend of convenience and community. Buyer profiles often include HDB upgraders, young professionals, and investors looking for a balance of capital appreciation and rental yield.

Outside Central Region (OCR): This region covers the suburban areas of Singapore, including districts 16, 17, 18, 19, 21, 22, 23, 24, 25, 26, 27, and 28. OCR properties are generally the most affordable, offering larger living spaces and catering primarily to owner-occupiers and first-time private property buyers. Government planning for the OCR emphasizes decentralization, with the development of regional centers like Jurong, Tampines, and Woodlands, bringing employment nodes and amenities closer to residents. This region attracts HDB upgraders, young families, and investors prioritizing lower entry prices and higher potential for percentage gains driven by infrastructure development and population growth.

Here's a simple comparison table summarizing the key characteristics of each region:

| Feature | Core Central Region (CCR) | Rest of Central Region (RCR) | Outside Central Region (OCR) |

|---|---|---|---|

| Key Districts | 9, 10, 11, Downtown Core, Sentosa | 3, 4, 5, 7, 8, 12-15, 20 | 16-19, 21-28 |

| Location | Prime City Centre | City Fringe | Suburban / Mass Market |

| Typical Buyers | Affluent Investors, Expats, UHNW | HDB Upgraders, Young Professionals, Investors | HDB Upgraders, Young Families, First-time Buyers |

| Investment Goal | Capital Preservation, Prestige, Strong Rental | Balanced Growth & Yield | Higher Percentage Gains, Affordability |

| Price Point | Highest | Mid-High | Most Affordable |

2. Singapore Property Market Overview

The Singapore private residential property market in 2026 continues to exhibit resilience, albeit with nuanced regional variations. The overall private residential price index rose by 0.9% in the first quarter of 2026, a pace similar to the average quarterly increase of 0.8% observed in 2025. This steady growth underscores the market's underlying stability despite global economic uncertainties. The rental market also saw a slight increase of 0.3% in Q1 2026, indicating sustained demand for leased properties.

New launch trends reveal a significant supply pipeline, with approximately 55,800 private residential units (including Executive Condominiums, ECs) expected to be completed in the coming years. Notably, the 1H2026 Government Land Sales (GLS) Confirmed List supply is 50% above the average half-yearly supply over the past decade, suggesting a proactive approach by the government to meet housing demand. This influx of new supply, particularly in the OCR, will be a critical factor influencing buyer behavior and price movements across regions.

Buyer behavior in 2026 is characterized by a continued focus on value and long-term growth. While local demand, particularly from HDB upgraders, has been a significant driver in the RCR and OCR, the CCR is seeing renewed interest due to a narrowing price gap with other regions. This suggests that discerning buyers are increasingly looking for opportunities in the prime segment as its relative value improves. Supply dynamics, coupled with evolving buyer preferences, mean that regional differences in performance are more pronounced than ever, making a granular understanding of each area essential for strategic investment.

3. OCR Explained

The Outside Central Region (OCR) is Singapore's largest residential segment, encompassing a wide array of suburban districts. These areas are characterized by a more relaxed pace of life, abundant green spaces, and a strong sense of community. Typical districts in the OCR include Woodlands, Hougang, Bedok, Punggol, and Jurong. The common buyer profiles in the OCR are primarily HDB upgraders, young families, and first-time private property owners who prioritize affordability, larger living spaces, and access to amenities like schools and neighborhood centers.

Advantages of OCR:

- Affordability: Generally offers the lowest entry prices per square foot, making private property ownership more accessible.

- Growth Potential: Significant government investment in infrastructure and regional hubs (e.g., Woodlands Regional Centre, Jurong Lake District) drives long-term capital appreciation.

- Family-Friendly: Abundance of schools, parks, and community facilities caters well to families.

- Higher Rental Yields: Often provides attractive rental yields, making it appealing for investors seeking cash flow.

Disadvantages of OCR:

- Longer Commute: Generally further from the CBD, leading to longer commute times for those working in the city center.

- Higher Supply Risk: The largest pipeline of new launches can sometimes lead to temporary oversupply, potentially moderating price growth in the short term.

- Lower Prestige: May not offer the same level of prestige or exclusivity as CCR properties.

Why OCR Remains Popular:

OCR remains highly popular due to its compelling value proposition. The ongoing decentralization strategy by the government, coupled with significant infrastructure developments like the Thomson-East Coast Line (TEL) and the Johor Bahru-Singapore Rapid Transit System (RTS) Link, has transformed many OCR areas into self-sufficient hubs. For instance, Woodlands is poised to become Singapore's Northern Gateway, with the RTS Link targeting operations by end-2026/early 2027, promising a 5-minute commute to Johor Bahru. Similarly, the Jurong Lake District is undergoing a massive transformation into Singapore's second CBD, attracting businesses and residents alike. These developments enhance connectivity, create job opportunities, and improve the overall liveability of OCR estates, making them attractive for both owner-occupiers and long-term investors.

4. RCR Explained

The Rest of Central Region (RCR) occupies a strategic position in Singapore's property market, bridging the gap between the prime CCR and the mass-market OCR. This city-fringe region offers a compelling blend of urban convenience and residential tranquility. Typical districts in the RCR include Tanjong Rhu, Queenstown, Kallang, Alexandra, and Paya Lebar. The common buyer profiles in RCR are often HDB upgraders seeking a more central location, young professionals desiring proximity to work and lifestyle amenities, and investors looking for a balanced risk-return profile.

Advantages of RCR:

- Strategic Location: Excellent connectivity to the CBD and other key employment hubs, often with shorter commute times than OCR.

- Balanced Growth & Yield: Offers a good balance of capital appreciation potential and attractive rental yields, making it a favorable option for many investors.

- Lifestyle Amenities: Access to a wide range of F&B, retail, and recreational options, often with a more vibrant urban feel than OCR.

- Urban Transformation: Many RCR areas are undergoing significant rejuvenation, such as the Greater Southern Waterfront, Paya Lebar Central decentralization, and Queenstown rejuvenation, driving future growth.

Disadvantages of RCR:

- Higher Entry Price: More expensive than OCR, potentially limiting affordability for some buyers.

- Competition: High demand can lead to competitive bidding and faster price increases, as seen in recent years.

- Smaller Units: Compared to OCR, units might be smaller due to higher land costs and density.

City-Fringe Appeal:

RCR's enduring appeal lies in its city-fringe location, offering the best of both worlds. Residents enjoy convenient access to the CBD and other central amenities without the premium price tag of CCR. This region is particularly attractive to HDB upgraders who are looking for a step up in lifestyle and investment potential, often driven by the strong appreciation of their HDB flats. The continuous development of integrated transport networks and lifestyle hubs further enhances RCR's attractiveness, making it a highly sought-after region for both owner-occupiers and investors.

5. CCR Explained

The Core Central Region (CCR) represents the pinnacle of Singaporean property, synonymous with luxury, exclusivity, and prime location. This region encompasses the most coveted addresses, including Orchard, River Valley, Marina Bay, Tanglin, and Bukit Timah. Properties here are often freehold, offering a sense of permanence and intergenerational wealth transfer. Common buyer profiles in the CCR include ultra-high-net-worth individuals (UHNWIs), foreign investors, and affluent local buyers seeking capital preservation, a prestigious address, and robust rental income from expatriate tenants.

Advantages of CCR:

- Prestige and Exclusivity: Unmatched status and a highly desirable address.

- Capital Preservation: Historically, CCR properties have demonstrated strong resilience during market downturns, making them ideal for wealth preservation.

- Strong Rental Market: High demand from expatriates and high-income professionals ensures stable and often higher absolute rental income.

- Limited Supply: Due to its prime location and established nature, new supply in the CCR is inherently limited, contributing to its scarcity value.

Disadvantages of CCR:

- Highest Entry Price: The most expensive region, requiring significant capital outlay.

- Lower Percentage Growth: While stable, CCR properties have shown lower percentage growth compared to RCR and OCR in recent years, particularly due to cooling measures impacting foreign buyers.

- Lower Rental Yield Percentage: Despite high absolute rents, the yield percentage can be lower due to the high purchase price.

Luxury Positioning:

CCR properties are defined by their luxury positioning, offering unparalleled amenities, bespoke services, and proximity to world-class shopping, dining, and entertainment. The government's strategic planning for the CCR reinforces its status as a global financial hub and a vibrant lifestyle destination. While foreign demand has been impacted by increased Additional Buyer's Stamp Duty (ABSD), the region continues to attract a steady stream of UHNWIs and returning Singaporeans who value its unique blend of sophistication and investment security. The narrowing price gap between CCR and other regions in 2026 presents a unique opportunity for astute investors to acquire prime assets at what could be considered a relatively undervalued position.

6. OCR vs RCR vs CCR Comparison Table

To provide a clearer picture of the investment landscape across Singapore's three property regions, the following table offers a comprehensive comparison based on key investment metrics:

| Feature | OCR (Outside Central Region) | RCR (Rest of Central Region) | CCR (Core Central Region) |

|---|---|---|---|

| Entry Price | Most Accessible (Lowest PSF) | Mid-High (Moderate PSF) | Highest (Premium PSF) |

| Rental Demand | Strong (Young families, local professionals) | Very Strong (Professionals, families, expats) | Strong (Expats, UHNWIs) |

| Capital Appreciation | Highest Percentage Growth (Historically) | Balanced, Consistent Growth | Stable, Wealth Preservation (Lower % Growth) |

| Family Appeal | High (Space, amenities, schools) | High (Connectivity, lifestyle, schools) | Moderate (Luxury, proximity to CBD) |

| Investor Appeal | High (Yield, long-term growth potential) | Very High (Balanced yield & growth) | High (Capital preservation, prestige) |

| Supply Risk | Higher (Largest new launch pipeline) | Moderate (Balanced new launch pipeline) | Lower (Limited new supply) |

Commentary:

The table highlights that each region caters to distinct investment objectives. The OCR offers the highest potential for percentage capital appreciation and rental yields, driven by affordability and ongoing urban development. However, it also carries a higher supply risk due to a larger pipeline of new launches. The RCR emerges as a "sweet spot," balancing reasonable entry prices with strong growth potential and attractive rental yields, making it highly appealing to a broad spectrum of buyers. The CCR, while offering the lowest percentage growth and yield, provides unparalleled capital preservation, prestige, and resilience, making it the preferred choice for wealth preservation and long-term stability.

7. Historical Performance Comparison

Analyzing historical performance patterns is crucial for understanding the long-term trajectory of Singapore's property regions. Over the past decade, the market has witnessed a significant shift in price dynamics, challenging traditional assumptions about regional superiority.

Historically, the CCR commanded a substantial premium over the RCR and OCR. However, data from recent years reveals a compelling narrative of narrowing price gaps. For instance, in 2015, the price gap between CCR and RCR was approximately 27%, while the gap between CCR and OCR was over 50%. Fast forward to 2026, and these gaps have compressed significantly. The CCR-RCR gap has narrowed to historically low levels, and the CCR-OCR gap has also seen a substantial reduction.

This compression is largely driven by the outperformance of the RCR and OCR. Over a 10-year period, OCR prices have soared by over 110%, and RCR prices have jumped by approximately 80%, while CCR prices have grown by a more modest 36%. This divergence in growth rates can be attributed to several factors:

- Decentralization and Infrastructure: Massive government investments in regional centers (e.g., Jurong, Woodlands) and transport networks (e.g., TEL, RTS Link) have significantly enhanced the appeal and value of OCR and RCR properties.

- HDB Upgrader Demand: A robust HDB resale market has empowered many Singaporeans to upgrade to private properties, primarily targeting the more affordable OCR and RCR segments, driving up demand and prices in these areas.

- Cooling Measures: Successive rounds of cooling measures, particularly the increase in ABSD for foreign buyers, have disproportionately impacted the CCR, which traditionally relied more heavily on foreign investment.

Practical Lessons:

The key takeaway from this historical analysis is that past performance is not always indicative of future results. The narrowing price gap suggests that the CCR may currently offer "fair value" or even be undervalued relative to its historical premium. Conversely, while the OCR and RCR have enjoyed stellar growth, buyers must carefully assess whether this momentum is sustainable, especially given the impending supply pipeline in the OCR. Investors should pivot from simply "buying cheap" to "buying value," recognizing that the best opportunities may lie in regions where the price-to-value ratio is most favorable.

8. Rental Demand Comparison

Rental demand is a critical component of property investment, providing cash flow and contributing to overall returns. The rental landscape in Singapore varies significantly across the three regions, reflecting different tenant profiles and market dynamics.

OCR Rental Demand:

The OCR rental market is primarily driven by local professionals, young families, and budget-conscious expatriates. Tenants are attracted to the OCR for its affordability, larger living spaces, and family-friendly amenities. Rental yields in the OCR are typically the highest among the three regions, often ranging from 3.5% to 4.5%. This strong yield is supported by consistent demand from those seeking value for money and a comfortable suburban lifestyle. Future demand drivers include the continued development of regional employment hubs, which will attract more professionals to live closer to their workplaces.

RCR Rental Demand:

The RCR enjoys robust rental demand from a diverse mix of tenants, including professionals, families, and expatriates who desire proximity to the city center without the premium cost of the CCR. The RCR offers a compelling balance of lifestyle amenities, connectivity, and relative affordability. Rental yields in the RCR are generally attractive, typically ranging from 3.0% to 4.0%. The region's resilience is bolstered by its broad appeal and the ongoing rejuvenation of city-fringe areas, ensuring a steady stream of prospective tenants.

CCR Rental Demand:

The CCR rental market caters to a niche but lucrative segment, primarily comprising high-income expatriates, senior executives, and UHNWIs. Tenants in the CCR prioritize prestige, luxury amenities, and unparalleled convenience. While the absolute rental income in the CCR is the highest, the rental yield percentage is often the lowest, typically ranging from 2.5% to 3.5%, due to the high capital value of the properties. However, the CCR rental market is known for its stability and resilience, often weathering economic downturns better than other regions due to the inelastic demand from its affluent tenant base.

9. Which Region Performs Best During Different Market Cycles?

Understanding how different regions behave during various market cycles is essential for risk management and strategic portfolio allocation.

Rising Markets:

During periods of economic expansion and rising property prices, the OCR and RCR typically exhibit the strongest percentage growth. This is driven by strong domestic demand, particularly from HDB upgraders, and the realization of infrastructure developments that enhance the value of these regions. The affordability of the OCR makes it highly responsive to positive market sentiment, leading to rapid price appreciation.

Flat Markets:

In flat or stabilizing markets, the RCR often emerges as the most resilient region. Its balanced appeal to both owner-occupiers and investors, coupled with its strategic location, provides a buffer against significant price corrections. The RCR's strong rental demand also offers investors a steady income stream, mitigating the impact of stagnant capital values.

Downturns:

During economic downturns or periods of market correction, the CCR historically demonstrates the greatest resilience. Properties in the CCR are often held by affluent individuals with strong holding power, reducing the likelihood of distressed sales. The inherent scarcity and prestige of CCR properties provide a floor to price declines, making it a preferred safe haven for capital preservation.

Recovery Phases:

As the market begins to recover, the CCR often leads the rebound, driven by opportunistic investors seeking undervalued prime assets. However, the RCR and OCR quickly follow suit as broader market confidence returns and domestic demand picks up. The pace of recovery in the OCR and RCR is often closely tied to the overall health of the economy and the employment market.

10. Where Are the Biggest Growth Opportunities Today?

Identifying the biggest growth opportunities requires looking beyond current pricing and focusing on areas undergoing significant transformation. In 2026, several key precincts stand out as prime candidates for future appreciation.

Woodlands Transformation:

Woodlands is undergoing a massive metamorphosis into Singapore's Northern Gateway. The centerpiece of this transformation is the Woodlands Regional Centre, a 100-hectare development projected to create 100,000 new jobs over the next 10 to 15 years. The imminent opening of the Johor Bahru-Singapore Rapid Transit System (RTS) Link, targeted for end-2026 or early 2027, will provide unprecedented cross-border connectivity, further enhancing the region's appeal. Projects like the upcoming Norwood Grand are well-positioned to benefit from this long-term growth trajectory.

Hougang Growth:

Hougang continues to evolve as a vibrant residential hub, supported by ongoing enhancements to its transport infrastructure and community amenities. The development of the Cross Island Line (CRL) will significantly improve connectivity, making Hougang an increasingly attractive option for homebuyers and investors seeking value in the OCR.

Bedok and Bayshore:

The Bayshore precinct is a major focal point for development in the East Coast. Envisioned as a 60-hectare residential district with over 12,500 new homes, Bayshore is transforming from a low-density enclave into a vibrant waterfront community. The recent opening of the Bayshore MRT station on the TEL has drastically improved connectivity, and the launch of projects like Vela Bay—the first new private launch in the area in over 25 years—signals strong growth potential.

Jurong Transformation:

The Jurong Lake District (JLD) is steadily progressing towards its vision as Singapore's second CBD. The government's commitment to developing integrated tourism attractions, commercial spaces, and residential projects in the JLD underscores its long-term potential. The release of significant GLS sites, such as the Town Hall Link White Site, highlights the scale of investment pouring into the region, promising substantial future upside.

Paya Lebar:

Paya Lebar Central has already established itself as a successful decentralized commercial hub. The future relocation of the Paya Lebar Airbase will unlock massive tracts of land for redevelopment, promising a new wave of transformation and growth in the surrounding RCR and OCR districts.

Original Analysis:

While the OCR presents compelling growth narratives driven by infrastructure, investors must carefully weigh these opportunities against the impending supply pipeline. The RCR, particularly areas benefiting from the Greater Southern Waterfront and Paya Lebar decentralization, offers a more balanced risk-reward profile. However, the most contrarian and potentially lucrative opportunity in 2026 might lie in the CCR. With the price gap between the CCR and other regions at historic lows, prime properties offer a rare combination of value, prestige, and capital preservation, making them an attractive proposition for astute investors looking beyond short-term trends.

11. Which Region Is Best for HDB Upgraders?

For HDB upgraders, the decision of which region to invest in is often a delicate balancing act between affordability, lifestyle aspirations, and long-term financial goals.

Affordability and Family Suitability:

The OCR remains the most practical and popular choice for the majority of HDB upgraders. Its lower entry prices allow families to acquire larger living spaces without overstretching their finances. The abundance of schools, parks, and family-centric amenities makes the OCR highly suitable for raising children. Furthermore, the ongoing development of regional centers ensures that residents have access to employment opportunities and lifestyle conveniences close to home.

Long-Term Upgrading Path:

The RCR presents an attractive alternative for upgraders with a slightly higher budget who desire a more central location and stronger capital appreciation potential. The RCR offers a significant lifestyle upgrade, with better connectivity to the CBD and a wider array of urban amenities. For many, the RCR represents the "sweet spot" in their upgrading journey, providing a balance of comfort and investment growth.

Recommendations:

- For budget-conscious families prioritizing space: The OCR is the clear winner. Focus on areas with upcoming infrastructure developments, such as Woodlands or Jurong, to maximize future upside.

- For professionals seeking a balance of lifestyle and investment: The RCR offers the best value proposition. Look for properties near major transport nodes or areas undergoing rejuvenation.

- For affluent upgraders focused on wealth preservation: While less common, the CCR can be an option for those who have accumulated significant equity in their HDB flats and prioritize prestige and long-term stability.

12. Which Region Is Best for Investors?

Investors must align their regional choices with their specific investment strategies, risk tolerance, and financial objectives.

Conservative Investors:

For investors prioritizing capital preservation and stable, albeit lower, rental yields, the CCR is the optimal choice. The inherent scarcity of prime properties and the strong demand from affluent tenants provide a robust defense against market volatility. The current narrowing price gap also presents a unique opportunity to acquire CCR assets at a relatively attractive valuation.

Growth Investors:

Investors seeking maximum capital appreciation should focus on the OCR and select areas within the RCR. The OCR, driven by massive infrastructure projects and decentralization efforts, offers the highest potential for percentage gains. However, this comes with higher volatility and supply risks. The RCR provides a more balanced approach, offering strong growth potential supported by solid fundamentals and broad buyer appeal.

Long-Term Investors:

For those with a long-term investment horizon, the RCR often provides the best overall returns. Its combination of steady capital appreciation, attractive rental yields, and strong tenant demand ensures a consistent performance over multiple market cycles. The RCR's strategic location and ongoing urban transformation make it a resilient and lucrative investment choice.

13. Case Studies

To illustrate the practical implications of investing in different regions, let's examine three hypothetical case studies based on typical new launch scenarios in 2026.

Case Study 1: Typical OCR New Launch (e.g., Woodlands)

- Purchase Price: $1.5 million for a 3-bedroom unit.

- Buyer Profile: A young family upgrading from an HDB flat, drawn by the affordability and the promise of the RTS Link and Woodlands Regional Centre.

- Potential Outcomes: The property offers excellent family living and strong potential for capital appreciation as the regional center develops over the next 10-15 years. Rental yields are expected to be healthy, providing good cash flow if the property is leased out. However, the buyer must be prepared for potential short-term price fluctuations due to new supply in the area.

Case Study 2: Typical RCR New Launch (e.g., Tanjong Rhu)

- Purchase Price: $2.2 million for a 3-bedroom unit.

- Buyer Profile: A mid-career professional couple seeking a balance of city-fringe convenience, lifestyle amenities, and solid investment returns.

- Potential Outcomes: The property provides a significant lifestyle upgrade and strong rental demand from expatriates and professionals. Capital appreciation is expected to be steady, supported by the area's established appeal and limited new supply. The investment offers a balanced risk-reward profile, making it a resilient addition to their portfolio.

Case Study 3: Typical CCR New Launch (e.g., River Valley)

- Purchase Price: $3.5 million for a 3-bedroom unit.

- Buyer Profile: A high-net-worth investor seeking capital preservation, a prestigious address, and a stable rental income stream.

- Potential Outcomes: The property serves as a secure store of wealth, with strong resilience during market downturns. While percentage capital growth may be lower than in the OCR or RCR, the absolute value appreciation can be significant. The property attracts high-quality tenants, ensuring a stable, albeit lower-yielding, rental income. The investment is viewed as a long-term legacy asset.

14. Common Mistakes Buyers Make

Navigating the Singapore property market can be complex, and buyers often fall prey to common pitfalls that can impact their investment outcomes.

- Chasing Prestige Over Value: Many buyers are drawn to the allure of the CCR without carefully assessing the price-to-value ratio. While prestige is important, overpaying for a prime address can severely limit future capital appreciation and rental yields.

- Ignoring Affordability: Stretching finances to purchase a property in a more expensive region can lead to significant financial stress, especially in a rising interest rate environment. Buyers must strictly adhere to their budget and factor in all associated costs, including maintenance and taxes.

- Misjudging Rental Demand: Assuming that all properties will easily attract tenants is a risky strategy. Buyers must thoroughly research the specific rental market dynamics of their chosen region, understanding tenant profiles, average yields, and potential vacancy risks.

- Buying Based Solely on PSF: Focusing exclusively on the price per square foot (PSF) can be misleading. A low PSF property might have a large, inefficient layout, resulting in a high overall quantum. Buyers must evaluate the total purchase price, layout efficiency, and overall value proposition.

Practical Advice:

Always conduct thorough due diligence, align your purchase with your long-term financial goals, and seek professional advice when necessary. Remember that the "best" region is the one that best suits your individual circumstances and investment strategy.

15. Frequently Asked Questions

1. Is OCR better than RCR?

Neither is inherently "better." OCR offers higher affordability and potential percentage growth driven by infrastructure, while RCR provides a better balance of central location, lifestyle, and steady appreciation. The choice depends on your budget and priorities.

2. Is CCR still worth buying in 2026?

Yes, especially for wealth preservation. The narrowing price gap between CCR and other regions makes it an attractive value proposition for investors seeking prime assets with strong resilience and prestige.

3. Which region has the highest rental demand?

All regions have strong demand, but they cater to different profiles. OCR attracts local families and budget-conscious expats, RCR appeals to professionals and mid-tier expats, while CCR targets high-income expats and UHNWIs. OCR generally offers the highest rental yield percentage.

4. Which region is best for HDB upgraders?

OCR is the most popular and practical choice for most HDB upgraders due to affordability and space. RCR is ideal for those with a higher budget seeking a lifestyle upgrade and better connectivity.

5. Which region has the best long-term growth?

Historically, OCR has shown the highest percentage growth due to decentralization. However, RCR offers the most consistent and balanced long-term growth, while CCR provides the best capital preservation.

6. How does the RTS Link affect OCR properties?

The RTS Link significantly boosts the appeal of OCR properties in the North, particularly Woodlands, by providing seamless cross-border connectivity, which is expected to drive long-term capital appreciation and rental demand.

7. Are city-fringe (RCR) condos overpriced?

While RCR prices have risen, they often represent a "sweet spot" offering city convenience without CCR premiums. Their strong demand and limited supply generally support their current valuations.

8. What is the impact of ABSD on the CCR market?

High ABSD rates for foreigners have cooled foreign demand in the CCR, leading to slower price growth compared to other regions. This has created a narrowing price gap, presenting opportunities for local buyers.

9. Should I buy a new launch or resale condo?

New launches offer modern facilities and progressive payment schemes but come at a premium. Resale condos offer immediate occupancy and established rental records, often at a lower PSF. The choice depends on your timeline and investment strategy.

10. How do government master plans influence property values?

URA Master Plans are crucial drivers of property values. Areas slated for significant infrastructure development, commercial hubs, or transport upgrades (like Jurong Lake District or Bayshore) typically experience strong capital appreciation.

11. Is it risky to invest in OCR due to high supply?

While OCR has the largest supply pipeline, this is often matched by strong demand from HDB upgraders. However, buyers should be selective, focusing on projects with unique selling points or proximity to key infrastructure to mitigate supply risks.

12. Can I get good rental yields in the CCR?

While absolute rental income is high in the CCR, the yield percentage is typically lower (2.5%-3.5%) due to high property prices. Investors in CCR usually prioritize capital preservation over high yields.

13. What makes the RCR a "Goldilocks" zone?

RCR is considered the "Goldilocks" zone because it offers a balance: it's not as expensive as CCR, but more central than OCR; it offers better yields than CCR, and more stable growth than OCR.

14. How important is proximity to MRT stations?

Proximity to MRT stations is a major factor in property valuation and rental demand across all regions, but it is particularly crucial in the OCR and RCR for commuting convenience.

15. Where can I find information on upcoming new launches?

You can find detailed information on upcoming projects through Upcoming Condo Launches Singapore 2026 and Upcoming GLS Sites, through reputable property portals and real estate agencies.

16. My View: Which Region Would I Choose Today?

As a property consultant analyzing the landscape in 2026, my perspective is shaped by the narrowing price gaps and the evolving dynamics of each region. There is no universally superior region; the optimal choice is deeply personal.

For Homebuyers and Families:

If I were advising a young family prioritizing space, community, and affordability, the OCR remains the most logical choice. The ongoing infrastructure developments, particularly in areas like Woodlands and the new Bayshore precinct, offer a compelling blend of lifestyle and future upside. The key is to select projects that are well-integrated with these new transport and commercial nodes.

For Investors:

For the pure investor seeking the best risk-adjusted returns, the RCR is my top pick. It consistently demonstrates the ability to attract a wide tenant pool, ensuring healthy rental yields, while its city-fringe location guarantees steady capital appreciation. It avoids the extreme price volatility sometimes seen in the OCR and the high entry barriers of the CCR.

For HDB Upgraders:

The decision for HDB upgraders hinges on their financial comfort zone. If the budget allows, stretching slightly for an RCR property often yields better long-term satisfaction and investment performance. However, a well-chosen OCR property near a major transformation hub is a highly prudent and profitable stepping stone.

The Contrarian Play:

Interestingly, the most compelling value proposition today might be in the CCR. The historical price gap between the CCR and the rest of the island has compressed to unprecedented levels. For buyers with the necessary capital, acquiring a prime, freehold asset in the CCR today is akin to buying blue-chip stocks at a discount. It's a play for wealth preservation and long-term legacy, capitalizing on a market anomaly that may not last.

Ultimately, the best region depends on the buyer's objectives, budget, timeline, and risk tolerance. The key is to move beyond generalized assumptions and focus on the specific value proposition of individual projects within these dynamic regions.

17. Conclusion

Navigating Singapore's property market in 2026 requires a nuanced understanding of the OCR, RCR, and CCR.

- Key Takeaways: The traditional price hierarchy is shifting. The OCR offers the highest growth potential driven by infrastructure, the RCR provides the most balanced risk-reward profile, and the CCR presents a unique value opportunity due to narrowing price gaps.

- Regional Strengths: OCR excels in affordability and family appeal; RCR shines in connectivity and balanced yields; CCR remains unmatched in prestige and capital preservation.

- Risks: OCR faces potential supply gluts; RCR requires careful project selection to avoid overpaying; CCR demands high capital outlay and offers lower percentage yields.

- Actionable Recommendations: Align your region choice with your specific goals. Families and budget-conscious buyers should explore OCR growth hubs. Balanced investors should target RCR city-fringe projects. Affluent buyers should capitalize on the current value in the CCR.

By carefully weighing these factors, you can make an informed and strategic investment decision that aligns with your long-term financial aspirations.

Ready to make your next property move? Schedule a free consultation with Jamus to discuss which region and property type best aligns with your investment goals and financial situation.